Canonical ESG Data Model

The authoritative semantic architecture for ESG and sustainability data.

CEDM (Canonical ESG Data Model) provides framework-independent, regulation-neutral infrastructure that enables organizations to model sustainability data once and report across GRI, ESRS, ISSB, TCFD, CDP, and emerging standards.

The Problem: ESG Data Fragmentation

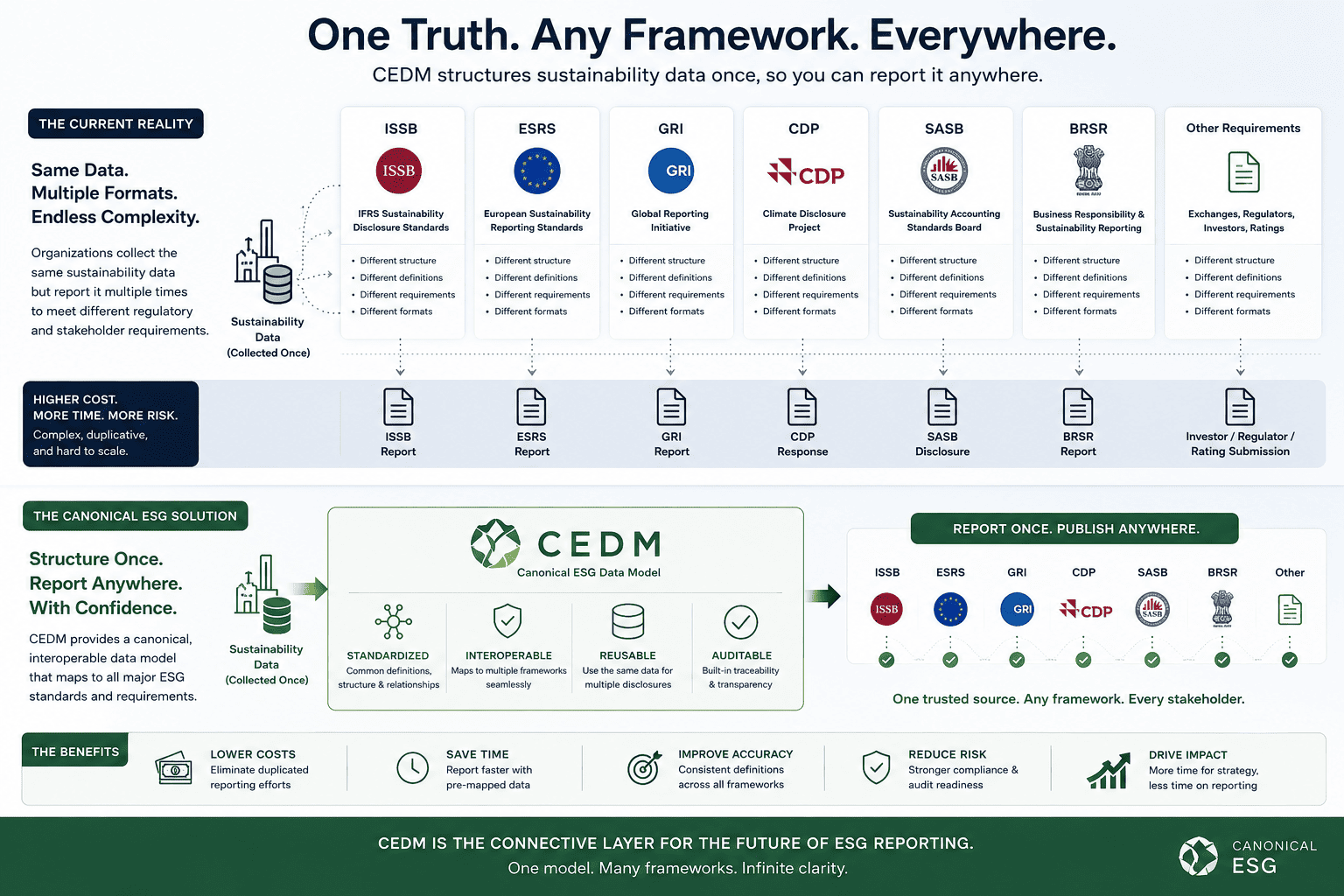

Organizations today face an unprecedented challenge: sustainability reporting has become a complex, multi-framework compliance exercise where the same underlying data must be restructured, reformatted, and reconciled across dozens of incompatible standards.

Framework Proliferation

Companies must report to GRI, ESRS, ISSB, TCFD, CDP, SASB, TNFD, and emerging jurisdictional standards—each with unique data structures, terminologies, and calculation methodologies. A single Scope 1 emissions figure may need to be reported in 5+ different formats.

Data Duplication & Reconciliation Burden

Organizations maintain parallel data pipelines for each framework, leading to duplicated effort, reconciliation errors, and audit complexity. A change to one data point requires manual updates across multiple systems and reports.

Regulatory Volatility

Frameworks evolve continuously. ESRS updates, ISSB amendments, SEC rule changes—each triggers costly system rewrites, data migrations, and process redesigns. Infrastructure built for one regulatory cycle becomes obsolete within 2-3 years.

No Semantic Interoperability

Existing frameworks do not share a common semantic foundation. Data cannot be exchanged, compared, or aggregated across systems without manual mapping and transformation. Investors, regulators, and stakeholders receive incomparable data.

Vendor Lock-In & Tool Fragmentation

Organizations are forced to adopt framework-specific software platforms that do not interoperate. Switching tools or consolidating systems requires complete data restructuring and workflow redesign.

The Result: ESG reporting has become a high-cost, low-value compliance exercise rather than a strategic data infrastructure. Organizations spend millions on reporting infrastructure that cannot adapt to regulatory change or support cross-framework analysis.

Why CEDM Was Created

CEDM was designed to solve the fundamental architectural problem in ESG data management: the absence of a stable, framework-independent semantic layer that can absorb regulatory volatility without destabilizing underlying data infrastructure.

Model Once, Report Everywhere

Organizations structure data using canonical semantic concepts (CDIs) that remain stable across framework evolution. Framework-specific reporting becomes a transformation layer, not a data restructuring exercise.

Absorb Regulatory Change Without Data Migration

When frameworks evolve, only the interpretation layer (CMPs) is updated—not the underlying data architecture. Organizations avoid costly system rewrites and data migrations.

Enable True Data Interoperability

By providing a common semantic foundation, CEDM enables data exchange between systems, platforms, and stakeholders without manual mapping or reconciliation.

Future-Proof ESG Infrastructure

CEDM is designed for a 10+ year stability horizon. Organizations can build reporting infrastructure that adapts to emerging standards without architectural rewrites.

Figure: How CEDM solves the multi framework reporting problem

Design Principles

Framework Independence

CEDM does not encode the logic of any single reporting framework. It provides neutral structures that can be mapped to any standard.

Semantic Stability

Data structures remain stable across regulatory cycles. Framework evolution is modeled through interpretation layers, not core architecture changes.

Regulation Neutrality

CEDM does not interpret regulations or assert compliance. It models structure, not legal requirements.

Long-Term Durability

Designed for 10+ year stability horizon. Versioning discipline ensures backward compatibility and migration clarity.

Three-Layer Architecture

CEDM operates through a disciplined three-layer architecture that maintains a clear separation between semantic meaning, framework interpretation, and regulatory application. This architectural discipline ensures that sustainability data remains stable and reusable across evolving reporting regimes.

Canonical Disclosure Intents (CDI)

The foundational semantic layer comprising 283 disclosure concepts that represent sustainability reporting requirements across 13 domains. Each CDI defines the meaning of a disclosure independently of any specific framework or regulation.

Representative Examples

CDI-CLIM-01Gross Scope 1 GHG emissions

CDI-GOVR-05Board oversight of sustainability matters

CDI-WORK-12Gender pay gap disclosure

CDI-BIOD-03Protected area interaction

Defining Characteristics

- Framework-neutral and jurisdiction-neutral — CDIs do not encode the logic of any single standard or regulatory regime

- Semantically stable (10+ year horizon) — Designed for long-term durability with minimal breaking changes

- Version-controlled (CDI v1 is frozen) — Immutable baseline ensuring reproducibility and audit integrity

- Non-authoritative — CDIs model structure and meaning; they do not interpret regulation or assert compliance

Canonical Mapping Packs (CMP)

Framework interpretation layers that establish explicit mappings between CDIs and the disclosure requirements of specific reporting standards. CMPs enable organizations to leverage a single semantic model across multiple frameworks without data duplication or reconciliation.

Supported Frameworks

GRI

Global Reporting Initiative

ESRS

European Standards

ISSB

International Standards

TCFD

Climate Disclosures

CDP

Carbon Disclosure Project

TNFD

Nature-related Disclosures

How CMPs Function

- Map framework requirements to CDIs — Establish explicit linkages between standard-specific disclosure requirements and canonical semantic concepts

- Document interpretive assumptions — Make professional judgments explicit and auditable

- Evolve independently from CDI semantics — Framework updates do not destabilize core semantic infrastructure

- Enable cross-framework comparability — Facilitate structural equivalence analysis and gap identification

Jurisdictional Mapping

Regulatory overlays that model how specific jurisdictions apply sustainability disclosure requirements within their legal and regulatory frameworks. This layer preserves semantic clarity while accommodating jurisdictional variation in materiality, scope, and enforcement.

Jurisdictional Capabilities

🇪🇺 EU CSRD Compliance Modeling

Double materiality, ESRS alignment, value chain scoping

🇺🇸 SEC Climate Disclosure Alignment

Materiality thresholds, Scope 3 triggers, safe harbor provisions

🇬🇧 UK Sustainability Requirements

TCFD-aligned disclosures, transition plan requirements

📊 Taxonomy Alignment

EU Taxonomy, China Green Bond, ASEAN Taxonomy

Architectural Principle: Regulatory logic is modeled transparently as an overlay without embedding jurisdictional requirements into core semantic structures. This ensures that CEDM remains regulation-neutral while supporting compliance modeling across diverse legal regimes.

What CEDM Provides

- •Canonical structures for metrics, targets, trajectories, and risks

- •Framework-agnostic data modeling patterns

- •Semantic foundation for cross-framework interoperability

- •Traceability, lineage, and audit transparency structures

- •Explicit versioning and backward compatibility discipline

- •Machine-readable schemas (JSON-LD, RDF)

What CEDM Does Not Do

- •Define disclosure requirements or materiality thresholds

- •Encode regulatory or jurisdictional compliance logic

- •Interpret external standards or assert compliance

- •Prescribe reporting formats or presentation requirements

- •Replace or supersede existing reporting frameworks

- •Provide legal or regulatory guidance

Core Components

Canonical Disclosure Intents (CDI)

283 semantic concepts representing disclosure requirements across 13 sustainability domains (climate, governance, economic, workforce, biodiversity, energy, materials, pollution, waste, water, affected communities, consumers, value chain workers).

CDIs provide stable semantic anchors that remain constant across framework evolution and regulatory cycles.

Canonical Mapping Packs (CMP)

Framework interpretation layers that map CDIs to specific reporting standards (GRI, ESRS, ISSB, TCFD, CDP, etc.). CMPs evolve independently from core semantics, enabling framework updates without architecture disruption.

Each CMP is versioned and frozen, ensuring reproducibility and audit traceability.

Data Structures & Schemas

Machine-readable specifications (JSON-LD, RDF) defining canonical structures for metrics, targets, trajectories, risks, evidence, and supporting metadata. Schemas support validation, interoperability, and automated processing.

Open-source schemas enable ecosystem integration and tool development.

Use Cases

Multi-Framework Reporting

Model sustainability data once using CEDM structures, then generate reports for GRI, ESRS, ISSB, TCFD, and CDP without data duplication or reconciliation.

Regulatory Transition

Maintain data continuity across regulatory changes. When frameworks evolve, update CMPs without restructuring underlying data architecture.

Data Interoperability

Enable data exchange between systems, platforms, and stakeholders using standardized semantic structures and machine-readable schemas.

Audit & Assurance

Support audit trails with explicit lineage tracking, evidence linkage, and version-controlled data structures that ensure reproducibility.

System Integration

Integrate sustainability data across ERP, GHG accounting, LCA, and reporting platforms using canonical data structures.

Future-Proofing

Build reporting infrastructure that adapts to emerging standards without architectural rewrites or data migration projects.

Technical Documentation

CEDM v1.0 Specification

ActiveComplete technical specification including data structures, semantic definitions, versioning protocols, and implementation guidance.

Current Version

v1.0.0

Released: 2024 | Status: Active

Coverage

283 CDIs

Across 13 sustainability domains

Framework Support

6+ Standards

GRI, ESRS, ISSB, TCFD, CDP, TNFD

Governance & Licensing

Open Standards

CEDM is published under Creative Commons Attribution 4.0 International (CC BY 4.0) license. Free to use, adapt, and distribute with attribution.

Schemas and reference implementations are open source (MIT License).

Governance

CEDM evolves through disciplined governance ensuring semantic stability, backward compatibility, and transparent change management.

Get Started with CEDM

Explore the technical documentation, review the CDI taxonomy, or contribute to the semantic infrastructure.

Non-Authoritative Reference Architecture

CEDM is a non-authoritative reference architecture developed in the public interest. It is not endorsed by, does not interpret, and does not represent any sustainability reporting standard, regulator, or jurisdictional authority. Organizations using CEDM remain solely responsible for compliance with applicable reporting requirements.